REGlobal presents an extract from Deloitte’s report titled Europe’s future aviation landscape: The potential of zero-carbon and zero-emissions aircraft on intra-European routes by 2040. The report highlights the technological advancements in aviation to achieve zero-carbon and zero-emission passenger aircrafts along with the future of aviation in the European countries.

The context for the decarbonization of the aviation sector

The need for disruption

Globally, aviation connectivity is a strong driver of economic growth, jobs, trade and mobility. At the same time, the growth in air traffic demand needs to be concomitant with maintaining high standards of aviation safety as well as reducing aviation’s environmental footprint. The aviation industry is one of many industries that has a heavy impact on global human-made emissions. While aviation accounts for 2-3% of global carbon emissions today, if no changes are made in the sector this will increase to as much as 27% by 2050. Based on planned reductions and “more efficient” fossil fuel technology, the industry is still projected to consume over 12% of the annual CO2 budget.

Increased public pressure

The past few years have seen an increase in public pressure on the sector, especially in Europe, with a growing media attention given to the “flight shaming” movement as well as discussions within different European governments about promoting a significant shift towards more sustainable modes of transport, such as rail. Under increased scrutiny, and following pledges made by other emission-intensive sectors, the European aviation sector adopted several resolutions to significantly reduce its emissions and a proposed approach to reach carbon-neutrality by 2050. To achieve these targets, the aviation industry is currently shifting from focusing solely on technological and operational improvements towards developing new systems and alternatives to kerosene to significantly reduce the emissions of the sector.

Powering aircraft sustainably

Energy efficiency improvements to current technologies, operations and infrastructure are part of the solution to decarbonize the aviation sector, but incremental improvements of existing systems won’t suffice to reach the decarbonization ambitions put forth by the EU Commission in its European Green Deal within reasonable timelines. As most of aviation emissions are related to the combustion of kerosene, it is crucial to focus on how airplanes are powered and uncover new and sustainable ways to propel aircraft.

Replacing kerosene with sustainable alternatives (also called Sustainable Aviation Fuels, or SAFs) could help reduce the net emissions of air travel, even in the short term. Indeed, technologies using biomass to produce jet fuels are already existing and several airlines started using biofuels (or a kerosene-biofuel blend) on different routes, including long-haul ones. However, scaling up the production of biofuels significantly (which currently represents less than 1% of global jet fuel demand) will increase the biomass demand, which in turn will lead to a critical competition for feedstock, land use, and water with other industries, such as food and feed production.

A solution potentially scalable would be to produce synthetic SAFs through the reaction of hydrogen and CO2. Hydrogen will need to be produced by using renewable energy to split water into hydrogen and oxygen, whereas CO2 will need to be captured from the air or as an output of industrial processes. However, the underlying technologies are yet to become cost competitive and it will take several years before the production of sustainable synthetic fuels is available at large-scale.

Most importantly, the combustion of SAFs still causes in-flight CO2 and NOx emissions that are similar to those of kerosene-powered aircraft and consequently SAFs only partially solve the sector’s environmental challenge. Scalable and truly sustainable innovation is required to reduce emissions from aviation and decrease the industry’s GHGs footprint in the long-term.

Batteries and hydrogen

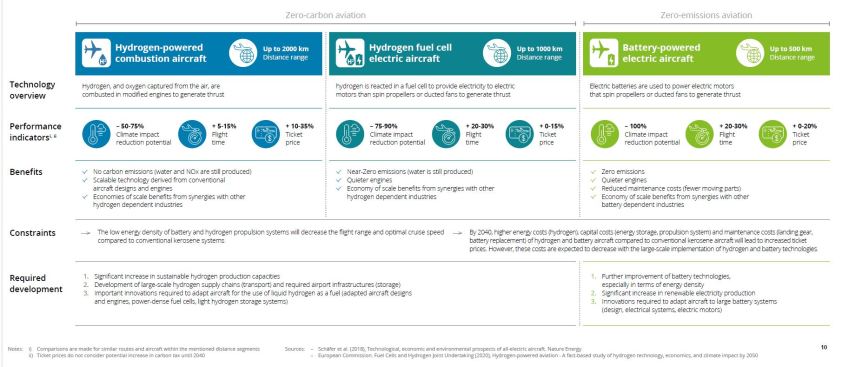

Promising technologies have emerged to help decarbonize the aviation sector in the long-term. The first one leverages recent advances in the automotive industry and consists of using batteries to power electric motors and spin propellers or ducted fans to generate thrust. While today’s battery energy densities can only power small aircraft for a short period of time, the current rate of improvement will make it possible for larger passenger aircraft to be powered by batteries for journeys of several hundreds and even thousands of kilometres in the future. The development of this technology is crucial, as battery-powered aircraft don’t produce any in-flight emissions, therefore removing any in-flight global warming effects. For a truly carbon neutral cycle, batteries need to be charged with renewable electricity.

Another promising solution to decarbonize aviation is to use hydrogen-based technologies. While hydrogen has been studied for decades, the growing share of renewable energy production has led to a particular interest in hydrogen as it can be used as an effective energy carrier or storage medium to mitigate the intermittent effects of solar or wind energy production. Hydrogen could therefore become the link between renewable energy and energy intensive industries, such as aviation.

Hydrogen can be used in two main ways to power aircraft: either in a fuel cell to provide electricity for electric motors (the same way as batteries), or by combusting it in modified jet engines to generate thrust. Hydrogen propulsion could significantly reduce the climate impact of the aviation industry by completely eliminating carbon emissions. It is, however, important to note that hydrogen propulsion technologies still emit water vapour and NOx (in case of combustion), which both promote non-CO2 related global warming effects (see dedicated section on the next page).

The busy short-haul mobility ecosystem

The current aviation technology roadmap suggests that such battery- and hydrogen-powered commercial passenger aircraft (also designated as zero-emissions and zero-carbon aircraft, respectively) will enter into service by 2040, with expected performances that would allow them to compete on the short haul market segment (with different key sub-segment for battery and hydrogen -powered aircraft). Given this, synergies with the road and rail sectors need to be considered.

From a road perspective, the recent progress in electric vehicle technologies has greatly extended the range and flexibility of EV cars and intercity buses. Whereas their potential for long-distance travel is limited, their immediate availability offers a concrete and cost-effective solution to reduce the climate impact of the transport sector. From a rail perspective, the development of the high-speed train network is likely to impose a significant competitive pressure on air transport. Furthermore, from an environmental point of view, current short-haul flights are typically much more carbon-intensive per kilometre than rail as a large proportion of an airplane’s fuel is burnt during the take-off and climbing phases (which represent a greater part of the flight on short routes). However, the extent to which the rail network can support a significant shift of passenger volumes from air to rail travel is uncertain and important infrastructure investment would be required to increase the network capacities.

The need for (EU & public) investments

On top of the ongoing discussions around the climate impact of aviation, the Covid-19 crisis highlighted the benefits of empty skies and highways on air quality and reinvigorated the debate on whether governments should use public money to bail out polluting industries, aviation included. While certain governments incorporated requirements to cut emissions in their funding agreements with airlines, or even ban flights shorter than 2 hours and 30 minutes where rail is available, public bailouts also need to address airlines’ unprecedented liquidity difficulties and long-term solvency challenge. Additional investments and policies supporting the development of zero-carbon and zero-emissions technologies for the aviation sector are therefore needed. However, support for these measures might compete with funds potentially allocated to the development of other sustainable transport or policies advocating for a modal shift, for example towards rail transport. While the current arguments in favour of electric vehicles and rail rely on their low climate footprint, the advent of zero-carbon and zero-emissions aircraft could significantly impact the discourse and drive government support for the aviation sector.

The road to zero-carbon and zero-emissions commercial passenger aircraft on intra-European short-haul routes

The road to truly zero-emissions aviation will take incremental steps, from making current aircraft more efficient, to replacing kerosene with hydrogen or integrating all-electric propulsion systems into new aircraft designs, while offsetting equivalent GHG emissions and introducing hybrid systems along the way. The different technologies will coexist for a certain period of time until a complete switch towards zero-carbon and zero-emissions aviation can be achieved.

Key features of zero-carbon and zero-emissions aircraft by 2040

Battery and hydrogen propulsion technologies represent the most promising paths towards a zero-carbon and zero-emissions aviation industry. While there is no all-round answer to decarbonize aircrafts’ operations, batteries and hydrogen can offer sustainable solutions across the different distance segments of the market. Therefore, this combination of technologies has the potential to greatly decrease the overall climate impact of the aviation sector.

Action is needed now

Zero-carbon and zero-emissions aircraft emerge as the best solutions to seamlessly transport a large number of passengers throughout Europe with a low climate impact.

As this report shows, zero-carbon and zero-emissions aircraft have the potential to cover a significant part of the Intra-EU passenger market by 2040, dates at which these technologies will enter into service. Avoiding the large emissions inherent to today’s kerosene aircraft while taking advantage of fast air travel at reasonable costs would drive zero carbon and zero-emissions aircraft away from current public concerns and provide a strong argument in favour of the development of air travel for the future. Even with decreased flight range compared to conventional kerosene aircraft, these future aircraft have the potential to cover up to 89% of the intra-EU market in 2040, representing a potential climate impact reduction of up to 59%.

When looking at different distance segments, the attractiveness of air travel on very short routes mainly depends on the rail network available on different routes. In case two cities are connected by an efficient high-speed rail network, travelling by rail can be faster than air. When less developed rail services are available, rail travel will be slower than air alternatives, and sometimes even road travel. Furthermore, the advent of all-electric VTOL and small aircraft in the coming years will also play a role in shifting parts of the ground commuting travel towards the air. On longer routes, the benefits of hydrogen propulsion aircraft are unequivocal, offering low emissions, prices in the range of other modes of transports, and travel times far below the ones of ground travel.

The broad aviation ecosystem needs to start cooperating today to ensure zero-carbon and zero-emissions aircraft will enter into service in time to meet the industry’s decarbonization targets.

Time is now of the essence to ensure these technologies are ready to enter the large-scale commercial passenger market within short timelines. With development times between 15 to 20 years and a broad deployment of large fleets usually taking up to 10 years, the aviation sector needs to invest significant resources today to develop the required innovations and technologies allowing the sector to reach the decarbonization objectives for 2050 set by the EU and ATAG. Policy makers, industries, and stakeholders from the broader aviation ecosystem need to cooperate to build the long-term regulatory and certification framework supporting the successful development of zero carbon and zero-emissions technologies. The remaining uncertainties around the extent of non-CO2 climate impact phenomena need to be clarified to allow clear target setting and development roadmaps that leverage the most efficient solutions. Laying out a long-term vision will strengthen the sector’s ability to plan the development of necessary technologies, as well as provide clarity as to where investments are most needed. Clearer perspectives will in turn attract funds more easily into innovation and pioneering R&D activities. On top of this, these new technologies will drive the need to develop supporting infrastructures, such as efficient battery charging/swapping systems at airports and large-scale hydrogen supply chains. Public support will therefore be fundamental in promoting both zero-carbon, zero-emissions technologies and infrastructure with targeted subsidies and economic measures to accelerate the competitiveness of these new sustainable aircraft.

Furthermore, the large-scale deployment of battery and hydrogen-powered aircraft will substantially increase the need for renewable energy production. Relying on non-renewable energy would greatly hinder the overall climate reduction potential of these aircraft and public entities must ensure that the future aviation sector can be supplied with sustainable energy, along with other sustainable modes of transports.

By removing the negative climate impact of air travel on short routes, zero-carbon and zero-emissions aircraft will significantly disrupt future mobility strategies and position aviation at the heart of the sustainable mobility ecosystem.

Repositioning aviation on very short-haul travels

Due to the synergies between battery-powered aircraft and other modes of transport on short routes of up to 500 km, targeted actions are required from policy makers to support the aviation industry in fully unlocking the immense potential of zero-emissions propulsion technologies

Whereas the benefits of hydrogen-powered aircraft over other modes of transport for routes of above 500 km is undeniable, distances below 500 km represent the most competitive segment for which both ground and air transport hold compelling benefits and where the existing infrastructure between two travels points has a significant impact on the advantage of a mode over another (i.e., efficient rail and road network, proximity to airports). The present report highlighted the significant benefits brought by electricity and battery-powered modes of transport (rail, EVs, battery-powered aircraft) on short distances in terms of low emissions and climate impact, while offering attractive travel costs and times. These three modes all represent promising solutions for the decarbonization of short-range mobility, but imply certain obstacles to their sole domination:

- Electric autonomous cars could become the most convenient mobility option on short distances, but road capacity challenges would be even more exacerbated than they are today with limited network expansion possibilities.

- A significant portion of travellers could shift to rail, but the same capacity constraints as for road would arise and the potential infrastructure investments could be significant to increase capacities only on targeted routes.

- Battery-powered airplane could represent a true game changer by offering a sustainable and fast travel option at attractive costs (which would further decrease in the future with new innovations and economies of scale). Furthermore, the limited infrastructure requirement needed to support battery swapping and charging systems would boost the development of the promising network of existing regional airports and unlock a seamless air travel over large geographies. Of course, the development of hydrogen aircraft for short routes also needs to be supported in parallel, as they would participate in the overall decarbonization of the 500 km segment by increasing the rate of kerosene aircraft replacement.

Therefore, policy makers need to strongly support the development of battery (and hydrogen) powered airplanes for the commercial passenger market on short routes and bolster the implementation of the required battery charging/swapping and hydrogen refueling infrastructure on large and regional airports. At the same time, the road infrastructure needs to be further optimized for EVs, policies encouraging carpooling have to be developed, and measures increasing the capacity of the rail network need to be taken. A first step would be to investigate the infrastructure requirements to integrate battery- and hydrogen-powered aircraft in the existing air network and compare them with investments required on the rail and road network to support a potential modal shift towards ground transport.

With the advent of zero-emissions aircraft on routes of up to 500 km, policy makers will need to define targeted mobility strategies that leverage the benefits of battery powered aircraft, rail, and electric vehicles based on infrastructure and mobility requirements.

The original report by Deloitte can be accessed by clicking here